Buying a home

Ameen Housing has helped hundreds of members buy homes in California. We invest up to one Million to help you buy your home.

investment

profitability

business

Buy a home, the halal way.

Our halal investments and home buying solutions are certified by the Assembly of Muslim Jurists of America (AMJA). Find your dream home without compromising your faith.

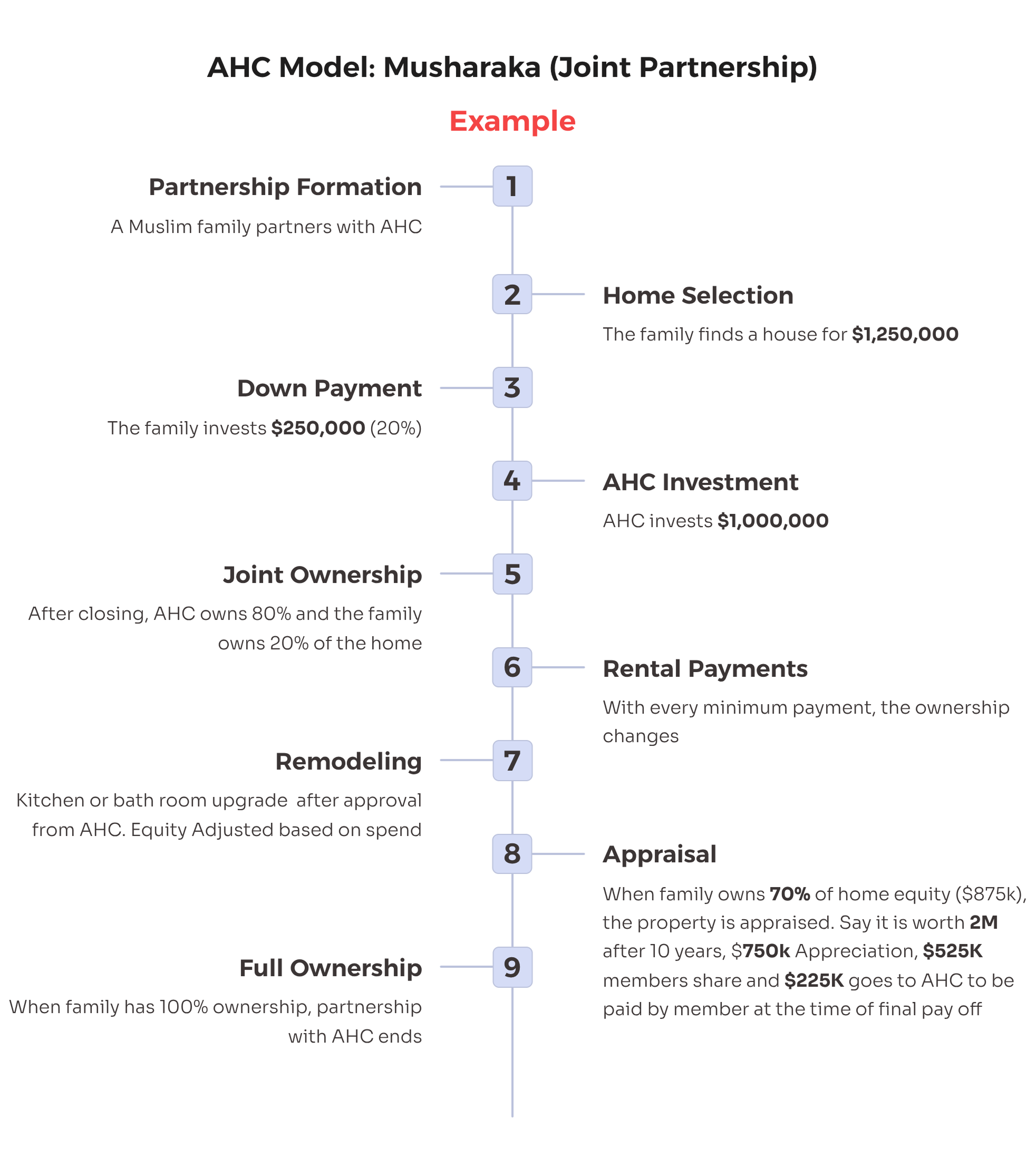

How it works

Get started today on your journey to buying a home that doesn’t compromise your faith. Here’s how our home buying process works:

- Members request that they be added to the Active List.

- Members' balance must be $100K or 10% of their intended purchase to make join the Active List.

- When the member reaches the #3 position on the Active List, the office will request that they deposit the full amount of their down payment.

- Members will then receive an occupancy letter to begin searching for a home.

For a full breakdown of how home ownership works, click this link to download the rules and regulations.

Begin your home buying process & become a member today

ApplyOur track record

AHC max $300K maximimum investment

AHC max $500K maximimum investment

AHC max $700K maximimum investment

AHC max $1.2M maximimum investment

Buying a home:

- Member balance must be $100K or 10% of the AHC investment whichever is less to be eligible for inclusion on the AL

- For investment less than US$100K, the member must have 10% of investment amount in his/her account at the time the RFAL is submitted and reviewed by the Board.

RFAL PROCESS

- A member intending to purchase/refinance a property needs to complete the RFAL form and mail it to the AHC Board for review. If the member is refinancing, proof of equity in home must be mailed along with the RFAL form.

- As per the Regulations of the Co-operative: "Members are NOT allowed to rent, lease or sublet ALL or PART of the housing unit."

- The member needs to have the minimum funds required for RFAL in his/her AHC account when submitting the RFAL to qualify.

- The date on which AHC receives the completed RFAL form will be the "ELIGIBILITY DATE" and will determine the position of members on the Active List.

- The AHC Board will review the RFAL form and will inform the member of their decision in writing or email.

- If the member's RFAL is denied, he/she will be informed in writing the reasons and the name will NOT be added to the AL.

- If the member's RFAL is approved, then:

○ The name of the member will be added to BOTTOM of thelist of ACTIVE members on the Active List.

○ A letter with member's position on AL will be mailed tothe member. - After the member's name has been added to the AL, the member will wait for other members, ahead of him/her on the AL, to move off the AL or get on "HOLD".

- When his/her name approaches the #3 position on the AL, AHC will contact the member to deposit his/her "FULL DOWN-PAYMENT", as indicated by the RFAL, within 30 days.

- If the member does NOT want to deposit additional funds at that time, then the person's name will be put on "UNQUALIFIED HOLD" and he/she will be asked to complete the RFAL Form.

- After the member has deposited his/her FULL required down-payment in to his/her AHC account, they will wait to have their name become #1 on the AL .

- Once the member's name has become #1 on the AL, the member will be asked to begin "OCCUPANCY PROCESS" so that he/she can either find and buy a home or refinance his/her home with AHC's total investment.

- A member has 60 days to find and purchase his/her new home.

- For refinancing a personal home mortgage, a member has 30 days to close the transaction.

- A member who has been asked by AHC to begin "OCCUPANCY PROCESS" may choose to be placed on "QUALIFIED HOLD" by informing the AHC Board using the RFAL Form.

- "HOLD" (QUALIFIED or UNQUALIFIED) is for a minimum of 45 days from the "HOLD DATE".

- Use the RFAL form to get on "HOLD" and to get "RE-ACTIVE on the AL "for both "Qualified Hold" and "Unqualified Hold".

- Use the RFAL form to be REMOVED from the AL.

TERMINOLOGY

ACTIVE LIST (AL) is the list of AHC members who have, in writing, informed AHC Board of their intentions to acquire/refinance a property with AHC's investment.

DOWN-PAYMENT is the investment balance REQUIRED by AHC in a member's. Eg. US$128K is the member's down-payment for AHC's investment of US$500K for a TOTAL investment of US$428K to purchase a new home. Use the Down-payment and AHC Investment Portion calculator to compute your investment.

TOTAL INVESTMENT is the total amount AHC will invest in a house. It is the sum of member's full Down-payment and AHC's Investment Portion investment. Eg. TOTAL investment isUS$428K to purchase a new home (US$128K is the member's down-payment + US$500K is AHC's investment portion).

AHC INVESTMENT PORTION is the amount that AHC invests in EXCESS of member's down-payment. Eg. AHC Investment portion is 500K, if the total investment isUS$428K and member's down-payment is US$128K.

ELIGIBILITY DATE is the date on which the RFAL or written/email notification requesting to be on Active List from the member is received by AHC.

HOLD DATE is the date on which the RHAL or written/email notification about going on"HOLD" from the member is received by AHC.

OCCUPANCY PROCESS is the final stage of receiving an AHC investment to close the deal.

QUALIFIED HOLD is the list of member name's on AL who were asked by AHC to begin OCCUPANCY PROCESS but instead chose to wait. A member on "Qualified Hold" HAS the full down-payment invested with AHC.

UNQUALIFIED HOLD is the list of member name's on AL who were asked by AHC to deposit their full down-payment but instead chose to wait. A member on the "Unqualified Hold" does NOT have the full down-payment invested with AHC.

RE-ACTIVE is to get active again after being on HOLD on the AL. Use the RFAL form

Replacing an existing mortgage:

The RFAL process is a streamlined and efficient process for an AHC member to add his/her name to the ACTIVE LIST. It is in the member's best interest to complete the RFAL Form carefully and completely with appropriate supporting documents so that his/her name is added to the AL quickly.

RFAL Requirements

AHC funds up to 80% of amounts US$100K and less, andup to 70% of higher amounts with a maximum of US$500,000.00 as "AHC INVESTMENT PORTION". The "DOWN-PAYMENT" (member's balance in his/her AHC account) is added to the "AHC INVESTMENT PORTION" to get the "TOTAL INVESTMENT".

Example:

- For US$100K investment from AHC, the member needs to have a "DOWN-PAYMENT" of US$25K. The TOTAL investment available for the member would be US$125K.

- For US$500K investment from AHC for refinancing a home,atleast 33K (10% of 333K) must be in member's AHC and the member's demonstrable equity in his/her home must be GREATER than US$66K (20% of US$333K). US$66K +US$33K= US$99K (30% US$333K). The TOTAL cash investment available for themember would be US$333K.

However, a member does NOT have to have the full "DOWN-PAYMENT" when requesting to have his/her name added to the"Active List".

TERMINOLOGY

ACTIVE LIST (AL) is the list of AHC members who have, in writing, informed AHC Board of their intentions to acquire/refinance a property with AHC's investment.

DOWN-PAYMENT is the investment balance REQUIRED by AHC in a member's AHC. Eg. US$128K is themember's down-payment for AHC's investment of US$500K for a TOTAL investment ofUS$428K to purchase a new home. Use the Down-payment and AHC Investment Portion calculator to compute your investment.

TOTAL INVESTMENT is the total amount AHC will invest in a house. It is the sum of member's full Down-payment and AHC's Investment Portion investment. Eg. TOTAL investment is US$428K to purchase a new home (US$128K is the member's down-payment + US$500Kis AHC's investment portion).

AHC INVESTMENT PORTION is the amount that AHC invests in EXCESS of member's down-payment. Eg. AHC Investment portion is 500K, if the total investment isUS$428K and member's down-payment is US$128K.

ELIGIBILITY DATE is the date on which the RFAL or written/email notification requesting to be on Active List from the member is received by AHC.

HOLD DATE is the date on which the RHAL or written/email notification about going on "HOLD"from the member is received by AHC.

OCCUPANCY PROCESS is the final stage of receiving an AHC investment to close the deal.

QUALIFIED HOLD is the list of member name's on AL who were asked by AHC to begin OCCUPANCY PROCESS but instead chose to wait. A member on "Qualified Hold" HAS the full down-payment invested with AHC.

UNQUALIFIED HOLD is the list of member name's on AL who were asked by AHC to deposit their fulldown-payment but instead chose to wait. A member on the "UnqualifiedHold" does NOT have the full down-payment invested with AHC.

RE-ACTIVE is to get active again after being on HOLD on the AL. Use the RFAL form to get "RE-ACTIVE on the AL". A member needs to deposit the FULL DOWN-PAYMENT to get "RE-ACTIVE" on AL from"UNQUALIFIED HOLD".

For Refinancing a member-owned home:

The member must either have:

- US$50K in his/her account at the time the RFAL, OR

- At least 10% of "TOTAL INVESTMENT" in member's AHCaccount (up to a maximum of US$50K). The member's "DemonstrableEquity" in his/her home combined with his/her AHC balance must be GREATERthan 30% of the "TOTAL INVESTMENT" being sought from AHC.

Eg. if a member wants AHC to refinance a mortgage of 200K, then the member musthave at least 20K in his/her AHC account and his/her equity in the home must begreater than 44K. For member's total investment of 66K (30% of 220K).

RFAL PROCESS

- A member intending to purchase/refinance a property needs to complete the RFAL form and mail it to the AHC Board for review. If the member is refinancing, proof of equity in home must be mailed along with the RFAL form.

- As per the Regulations of the Co-operative: "Members are NOT allowed to rent, lease or sublet ALL or PART of the housing unit."

- The member needs to have the minimum funds required for RFAL in his/her AHC account when submitting the RFAL to qualify.

- The date on which AHC receives the completed RFAL form will be the "ELIGIBILITY DATE" and will determine the position of members on the Active List.

- The AHC Board will review the RFAL form and will inform the member of their decision in writing or email.

- If the member's RFAL is denied, he/she will be informed in writing the reasons and the name will NOT be added to the AL.

- If the member's RFAL is approved, then:

○ The name of the member will be added to BOTTOM of thelist of ACTIVE members on the Active List.

○ A letter with member's position on AL will be mailed tothe member. - After the member's name has been added to the AL, the member will wait for other members, ahead of him/her on the AL, to move off the AL or get on "HOLD".

- When his/her name approaches the #3 position on the AL, AHC will contact the member to deposit his/her "FULL DOWN-PAYMENT", as indicated by the RFAL, within 30 days.

- If the member does NOT want to deposit additional funds at that time, then the person's name will be put on "UNQUALIFIED HOLD" and he/she will be asked to complete the RFAL Form.

- After the member has deposited his/her FULL required down-payment in to his/her AHC account, they will wait to have their name become #1 on the AL .

- Once the member's name has become #1 on the AL, the member will be asked to begin "OCCUPANCY PROCESS" so that he/she can either find and buy a home or refinance his/her home with AHC's total investment.

- A member has 60 days to find and purchase his/her new home.

- For refinancing a personal home mortgage, a member has 30 days to close the transaction.

- A member who has been asked by AHC to begin "OCCUPANCY PROCESS" may choose to be placed on "QUALIFIED HOLD" by informing the AHC Board using the RFAL Form.

- "HOLD" (QUALIFIED or UNQUALIFIED) is for a minimum of 45 days from the "HOLD DATE".

- Use the RFAL form to get on "HOLD" and to get "RE-ACTIVE on the AL "for both "Qualified Hold" and "Unqualified Hold".

- Use the RFAL form to be REMOVED from the AL.

TERMINOLOGY

ACTIVE LIST (AL) is the list of AHC members who have, in writing, informed AHC Board of their intentions to acquire/refinance a property with AHC's investment.

DOWN-PAYMENT is the investment balance REQUIRED by AHC in a member's. Eg. US$128K is the member's down-payment for AHC's investment of US$500K for a TOTAL investment of US$428K to purchase a new home. Use the Down-payment and AHC Investment Portion calculator to compute your investment.

TOTAL INVESTMENT is the total amount AHC will invest in a house. It is the sum of member's full Down-payment and AHC's Investment Portion investment. Eg. TOTAL investment isUS$428K to purchase a new home (US$128K is the member's down-payment + US$500K is AHC's investment portion).

AHC INVESTMENT PORTION is the amount that AHC invests in EXCESS of member's down-payment. Eg. AHC Investment portion is 500K, if the total investment isUS$428K and member's down-payment is US$128K.

ELIGIBILITY DATE is the date on which the RFAL or written/email notification requesting to be on Active List from the member is received by AHC.

HOLD DATE is the date on which the RHAL or written/email notification about going on"HOLD" from the member is received by AHC.

OCCUPANCY PROCESS is the final stage of receiving an AHC investment to close the deal.

QUALIFIED HOLD is the list of member name's on AL who were asked by AHC to begin OCCUPANCY PROCESS but instead chose to wait. A member on "Qualified Hold" HAS the full down-payment invested with AHC.

UNQUALIFIED HOLD is the list of member name's on AL who were asked by AHC to deposit their full down-payment but instead chose to wait. A member on the "Unqualified Hold" does NOT have the full down-payment invested with AHC.

RE-ACTIVE is to get active again after being on HOLD on the AL. Use the RFAL form

What Makes AHC's process Halal?

What is the key differentiator between AHC's Investment System and conventional mortgages?

One of the primary condition that makes any financial contract acceptable, from the Shariah perspective, is that, "the parties involved agree to participate in both the GAIN and the LOSS that may result from such an investment". Any contract that is missing this clause is "not acceptable" from a Shariah perspective. In the conventional mortgage systems, lenders never agree to share the loss with the homeowner and hence are not Islamically acceptable and permissible. AHC in principle and as a part of its contract agrees to bear the losses with the homeowner in the same ratio it agrees to share in the gains. This differentiates AHC from all other conventional mortgage and financing systems and makes the acceptable as per the Shariah. Besides this, the second key problem from a Shariah perspective in the financial contract with the conventional financing systems is the agreement to pay interest at certain agreed rate. This is outright Haram. In the AHC contract the RENT (not interest) is decided based on the fair market rental value of the property and AHC's share or rent is dependent on its equity. The homeowners share of the rent is used to purchase more equity from AHC. This from an Islamic perspective is 100% legitimate.

Why is the rent that AHC collects not considered interest? Banks lend at variable rates which can change with the market conditions and demand...There are two important concepts that have to be clearly understood:

1. PROFIT: Income from use of an ASSET or income from trading a permissible COMMODITY.

2. USURY: Income from use of MONEY...

and Allah has permitted trading and forbidden usury..."

Al-Quran, Surah Al-Baqarah (Chapter 2; Verse 275)

Consequently, the Shariah permits PROFIT but prohibits USURY. Bank's income is derived from the use of money by the borrower, which is prohibited. AHC invests in the property and derives its income from the compensation given by the user for the use of that property. This is perfectly halal.

Banks do take losses in case of foreclosures and bankruptcies, so they are fulfilling the condition of participating in losses. Why are they then not OK?

Yes, they do take those losses in case of foreclosures only when you file for bankruptcy and there is no other way left for them to get to your other assets. As we mentioned above the condition that makes a contract legitimate Islamically is "Agreeing and Willing to take part in the loses as well as the profits". The bank in this instance was forced to take a loss but it had never agreed to take a loss. Had it agreed to take the losses as AHC, you would get back a portion of your equity minus the losses.

by the BORROWER.

the outstanding LOAN.

NO appraisal is needed.

For further information against riba please read Sheikh Maulana Abul Ala Maududi's Opinion AGAINST RIBA based on Prophet Muhammad's (P&BUH) Sunnah and Ahadith